Saturday, August 30, 2025

ZZ25027 SpaceX Starship Rocket Success V01 300825

Thursday, August 28, 2025

ZZ25026 AI and Cancer Diagnostics V01 280825

Tuesday, August 26, 2025

ZZ25025 Nvidia Results V01 270825

ZZ25024 Filtronic and SpaceX V01 270825

Sunday, August 24, 2025

ZZ25023 AI and Marketing V01 250825

When the dust settles on President Trump’s latest round of tariffs, growth is going to be slower, inflation more stubborn, and interest rates still higher than many people thought.

And that means one thing: the need for efficiency and for technological transformation — particularly in a slower-growth region like Europe — will be more important than ever. As a result, AI implementation is set to only get faster.

Nowhere is that the case more so than in marketing, where AI has begun to upend the way brands create their advertising and is set to transform how consumers find products to buy.

Two years ago we identified five areas where AI would impact the advertising business: visualisation and copywriting; hyperpersonalisation at scale; media planning and buying; general efficiency; and the democratisation of knowledge.

We are seeing those in full swing, and we have already moved forward from generative content creation — where AI responds to the instructions it is given — to agentic content, created by AI with minimal human involvement. Our Puma commercial in March this year led the way, training a team of AI agents to create the advertising from beginning to end, designing preliminary concepts, writing scripts, generating high quality video and pulling it all together in a finished commercial. We’re doing the same for GM, General Mills and Google Pixel. What this means for clients is that instead of spending £2.5 million and four months to make a commercial, you can do it for £500,000 in a couple of weeks.

So it’s no surprise that companies who are facing a world of uncertainty, slow growth and the impact of tariffs are looking seriously at reducing their costs by using AI at scale.

“If you’re a brand or a retailer there willl be a whole set of different challenges

One thing this does mean is that the way agencies are remunerated has to change: we have to switch from charging for time, which is hugely compressed by AI, to charging for results, what matters to the marketer. We’re just at the beginning of that.

The technology itself is moving at lightspeed: companies like Runway, Luma and Minimax that have emerged in this space are raising billions of dollars through initial public offerings and fundraising.

And the quality of what the technology can deliver is also improving rapidly. You can see a dramatic difference between content created just two or three months ago and what we’re doing today.

With all the large language models (LLMs) one thing is clear: the more data you feed in, the better results you get. There will be hallucinations, and at the same time AI does pose an existential threat, as we face the prospect of machines becoming more powerful than humans. But none of this will stop the onward march of AI and the demand for more efficiency will only drive it forward.

The other side of the marketing coin is consumer behaviour and how quickly shoppers will adopt AI to help them make purchases, specifically if and when they will switch from search to using an AI agent. So the current websitebased marketing system for consumer products may be revolutionised by that.

It poses a dilemma for Google since it introduced Gemini 2.0 late last year. It has enormous revenues from search-based advertising, and it’s not clear what the revenue model would be from an agentic approach to finding and buying products. For now, Google says that agents have increased the demand for search, and I think that’s true, but at some point people will switch to directly using the agent instead of search.

If you’re a brand, or a retailer, there will be a whole set of opportunities and challenges. An LLM can understand the context and detail of what a consumer is looking for better than search.

Marketers will need to disseminate better information more widely to ensure that their product gets the consideration it deserves.

Trump’s imposition of 100 per cent tariffs on chip imports to the US — subject to some big carve-outs — is unlikely to slow the march of AI, and if anything will make both the US and China go even faster. He wants production to be switched to the US, but what we are seeing is the emergence of two systems, one for the West and one for China.

Finally, if you need evidence of the power of AI to boost efficiency and cut costs, look at the recent pronouncement of data analytics firm and AI powerhouse Palantir, which has just recorded its first $1 billion quarter, and whose chief executive, Alex Karp, has promised to boost revenue tenfold at the same time as shrinking his workforce by more than 10 per cent, from 4,100 to 3,500. He sees Palantir as the bridge that allows businesses to realise the benefits from LLMs. On the face of it, the ambition is incredible — but there’s a lot of people who believe they can do it.

Sir Martin Sorrell is founder and executive chairman of the digital advertising and marketing services business S4 Capital

ZZ25022 Palantir Technologies. V01 250825

What Does Palantir Technologies Do?

Palantir Technologies Inc. is a publicly traded American software company, founded in 2003 and headquartered in Denver, Colorado . It specializes in platforms that enable deep data integration, analysis, and operational insights—used extensively by both government and commercial organizations.

Core Platforms

• Palantir Gotham

Built for intelligence, defense, and law enforcement agencies, Gotham helps integrate and analyze vast, structured and unstructured datasets—from surveillance feeds to reports from informants. It’s used for discovering patterns, creating intelligence insights, and supporting mission-critical, real-world decision-making .

• Palantir Foundry

This enterprise-focused platform integrates disparate data sources—like ERP systems, IoT devices, and more—into a unified environment. It allows non-technical users to build dashboards, models, and workflows, aiding tasks such as supply chain optimization, predictive maintenance, and risk management. It’s widely adopted in sectors like healthcare, finance, energy, manufacturing, and even aerospace .

• Palantir Apollo

Launched in 2022, Apollo is Palantir’s orchestration engine, enabling continuous deployment, updates, and management of Gotham and Foundry across cloud, on-premises, edge devices, and even classified networks. It facilitates DevOps and CI/CD processes in complex environments .

• Palantir Artificial Intelligence Platform (AIP)

AIP provides unified access to large language models (LLMs)—across open-source, self-hosted, and commercial sources. It integrates AI into structured and unstructured data workflows, offering tools such as virtual assistants, AI-driven task automation, and orchestrated AI agents—while maintaining reliability and corporate guardrails .

Business Model & Market Reach

• Revenue Streams

Palantir operates through two main revenue streams:

1. Government Contracts – Includes U.S. federal agencies (e.g., Defense, Intelligence, ICE) and international allied governments.

2. Commercial Clients – Encompasses industries such as finance, manufacturing, energy, healthcare, and more .

• High-Touch Integration

Rather than off-the-shelf SaaS, Palantir heavily invests in onboarding and customizing its solutions for each client. These multi-year, deeply embedded contracts result in high gross margins and strong client retention—but can limit scalability and cause lumpy revenue quarters .

Real-World Usage Examples

• Defense & Intelligence

Gotham has been credited with aiding major operations—some reports even link it indirectly to events like the capture of Osama bin Laden . It’s also used for geospatial tracking, anti-terrorism, counterinsurgency, and battlefield awareness .

• Government & Health

Foundry enabled data management and decision-making during the COVID-19 pandemic—optimising resource allocation and vaccine distribution in several countries . In the UK, Palantir has also engaged in NHS-related data programs, including COVID data stores and proposals for a federated data platform, though not without criticism from civil liberty groups .

• Commercial Applications

• Airbus used Foundry (via the Skywise platform) to streamline A350 production by aggregating 400 data sources across the supply chain .

• Ferrari employed Foundry to analyze car-system data for real-time maintenance and performance optimization.

• Firms like Credit Suisse and BP have used the platform for risk analytics and efficiency gains .

• Immigration Enforcement

Palantir is developing ImmigrationOS—a $30 million contract with U.S. Immigration and Customs Enforcement (ICE)—to identify, track, and potentially deport undocumented individuals. This project, with expected rollout by late 2027, raises significant privacy and civil liberties concerns .

• Financial Services

Processing huge datasets for analysis, Palantir helps clients like Citi modernize their wealth management platforms with real-time insights and streamlined onboarding .

Controversies & Challenges

• Ethical and Privacy Concerns

Palantir has been widely criticized for its role in government surveillance, immigration enforcement, and data aggregation—prompting debates over civil liberties and ethical boundaries .

• Valuation Debates

Despite strong contracts and growth, analysts frequently note that Palantir’s stock valuation is lofty compared to fundamentals, with concerns over its ability to sustain investor expectations, especially given broader macroeconomic volatility in AI and tech stocks .

Summary Table

Platform / Aspect Purpose & Use Case

Gotham Government intelligence, defense, law enforcement

Foundry Enterprise data integration and analytics across industries

Apollo Software deployment/orchestration across environments

AIP AI-driven models and automation with built-in guardrails

Business Model High-touch, contract-based with segments in gov’t & commercial

Key Clients U.S. agencies, ICE, airlines, automakers, financial firms, NHS

Main Controversies Surveillance, ethics, valuation concerns

Palantir positions itself uniquely at the intersection of intelligence-grade software and enterprise analytics, offering powerful platforms that unify data, enable rapid insight, and drive real-world operations—from battlefield logistics to corporate strategy.

Would you like to explore a particular domain—such as their AI platform (AIP), ethical implications, or financial performance—in more detail?

ZZ25021 Apple iPhone Cameras and Lenses V01 240825

The iPhone camera system is the result of Apple’s integration of hardware, software, and suppliers. Here’s how it breaks down:

📷 Camera Lens & Hardware Manufacturers

Apple designs the camera module architecture itself, but it relies on specialized suppliers to make key parts:

• Lens suppliers:

• Largan Precision (Taiwan) – the primary supplier of iPhone camera lenses.

• Genius Electronic Optical (GSEO) (Taiwan) – also supplies lenses for iPhones.

• Sunny Optical (China) – has supplied some lenses in recent years.

• Image sensors:

• Sony – Apple has used Sony’s CMOS image sensors in iPhones for years. These sensors capture the raw image data before Apple’s software processing.

• Camera modules (assembly):

• Companies like LG Innotek (South Korea) and Sharp (Japan) assemble the full camera module, combining lenses, sensors, and stabilizers.

💻 Camera Software & Processing

• Apple develops all camera software and image processing algorithms in-house.

• The iPhone’s ISP (Image Signal Processor) is part of the Apple-designed A-series chips (e.g., A16 Bionic, A17 Pro).

• Apple’s software stack includes:

• Smart HDR (for balancing highlights and shadows).

• Deep Fusion (machine learning-based detail enhancement).

• Photonic Engine (improved low-light processing).

• ProRAW & ProRes formats (for professional photography and video).

So while Sony and lens makers provide the hardware, the “look” of iPhone photos—color science, tone mapping, night mode, cinematic mode—is largely due to Apple’s proprietary software and silicon.

✅ In short:

• Lenses: Largan, GSEO, Sunny Optical.

• Sensors: Sony.

• Modules: LG Innotek, Sharp.

• Software & ISP: 100% Apple.

Would you like me to also map out how this supply chain has shifted over the years (e.g., which companies Apple has leaned on more recently)?

ZZ25020 MIT.nano V01 240825

Advancing nanoscale science and engineering

MIT.nano was designed as a vessel to explore the dawn of the Nano Age. Located in the Lisa T. Su Building at MIT, we are a shared resource for the entire campus, an open-access, service-oriented facility located in the heart of MIT. Any faculty member, researcher, and student—as well as qualified users from industry, academia, and government—may bring a project or unsolved problem to our specialized environments and conduct their work supported by highly qualified technical staff.

We are open access.

Researchers from MIT constitute our primary user community; individuals from other academic institutions, industry collaborators, consortium member companies, and other external organizations are also welcome. Every step of the way, our staff are here to enable researchers and educators to get their work done with as few barriers to progress as possible.

We offer a broad set of advanced capabilities.

Sharing resources through MIT.nano enables the MIT community to acquire the state-of-the-art equipment that would be challenging for individual labs or departments to afford or maintain on their own. The ample size of our research facility also allows us to look beyond the present state-of-the-art by seeding dedicated lab spaces where new nanoscience and nanotechnology tools, instruments, processes, and techniques can be reinvented.

We make connections, on and off campus.

Through its central location on campus, the facility is a natural convening place for interdisciplinary research. At MIT.nano, electrical engineers, mechanical engineers, and physicists work alongside—and collaborate with—biologists, materials scientists, chemists, software engineers, artists, and others. Through initiatives such as the MIT.nano Consortium, we engage with leading companies that span industries from around the world. MIT.nano's programs and initiatives create opportunities to focus interdisciplinary teams on urgent challenges.

We’re proud to serve this special community. The collective imagination, passion, and talent of our diverse researchers will advance the frontiers of knowledge and usher the world into the Nano Age.

If you are a researcher interested in using the facilities and tools of MIT.nano, visit our user portalto get started.

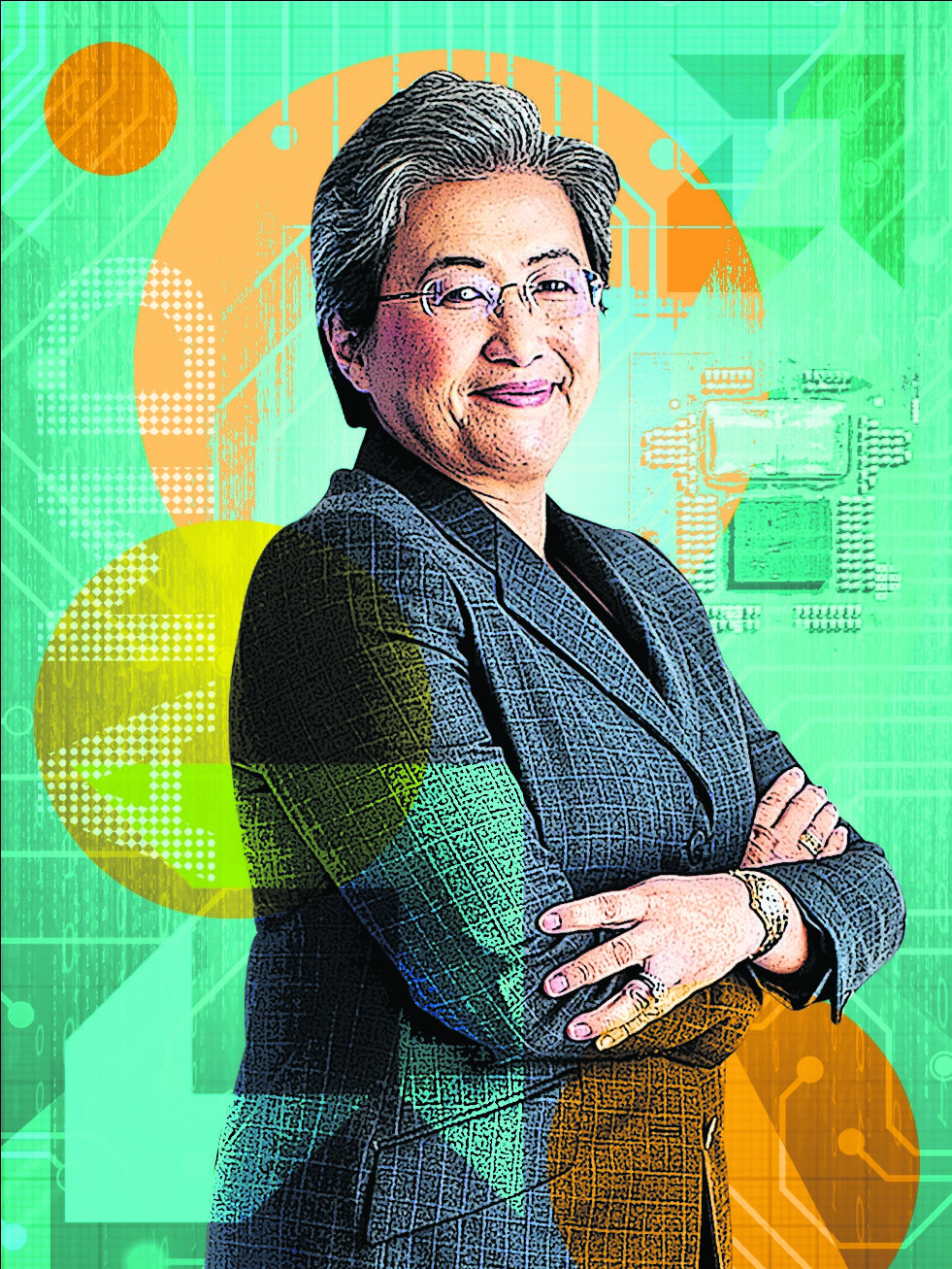

ZZ25019 AMD Chips V01 240825

Before Lisa Su walks into the room, a flurry of nervous activity unfolds. An assistant scuttles in to place two chilled bottles of her favoured brand of water — Fiji — where she is expected to sit.

A PR handler warns against probing into the personal life of the chief of Advanced Micro Devices (AMD), America’s biggest semiconductor company after Nvidia and Broadcom. “If you start getting one word answers, then ... I just want to make sure it’s as productive a discussion as possible,” he says nervously.

In the foyer lurks her mustachioed security guard, a man with arms larger than my thighs. Moments later, the press attaché pops his head back into the room: “She’ll be arriving shortly.”

For all the commotion, Su, 55, does not come off as a diva. “Nice to see you,” she says as she walks in, wearing a blue blazer, white trainers and toting (yet another) bottle of Fiji water. The interview is only one hour long; she will not go thirsty.

Su is not exactly warm but not cold either. Rather, she is serious. A serious woman in a very serious job, the daughter of immigrant parents, an MIT engineer who climbed the greasy pole of corporate America to run what is today one of the most important companies in the world.

In November 2022, OpenAI launched ChatGPT and triggered a multitrilliondollar race to build data centres as the world was swept up in the artificial intelligence revolution. The critical piece — the brains of these systems — are the meticulously engineered wafers of silicon packed with billions of transistors made by the likes of AMD.

Profits for the first half of the year jumped fivefold to $1.6 billion on $15.1 billion in sales, up 33 per cent on the same period last year. Its surging share price — the stock closed on Friday at $167.76 — pushed its market value to $272 billion.

That makes AMD, which employs 29,000 people globally, far larger than Britain’s biggest public company, the drugs giant AstraZeneca, and well over double the value of Intel, its stumbling US rival.

AMD is not, of course, Nvidia, the $4.3 trillion behemoth run by Su’s “distant” cousin Jensen Huang — that family relationship is another area on which I am told not to tread. But this is the best time to be in the semiconductor business since the dawn of the personal computer — perhaps better. And Su, having executed a decade-long revival of AMD, has put it in prime position to reap the rewards of the AI-ification of everything.

The world wants digital brains and that is what she is selling. This moment has also vaulted her, and AMD, to the centre of the geopolitical stage. She and Nvidia’s Huang made news this month when they struck an export deal with President Trump.

In exchange for handing a 15 per cent cut of all their China sales to the US government, Trump carved them out of a national security ban that restricted chip sales to China. Did she hammer out that deal personally with The Donald?

“I’m not going to get into all of the back and forth,” she says diplomatically. But it is, “very safe to say”, she says, that she is spending a lot more time in Washington than she used to. “I actually do believe AI is a race and it’s a race to intelligence. It’s a race to capability. So every country is now thinking about how do they have their own AI policy and AI plans?”

Critics bashed the profit-sharing arrangement as “crony capitalism”. Su won’t take that bait. “Where do you draw the line of what is national security versus what is, you know, just having more people in your ecosystem. I think we found the right balance.”

It must be said that both Nvidia and AMD are selling chips specially designed for the Chinese market with certain computing and memory capabilities “turned off” to make them less powerful.

Beyond politics, however, Su is a techno-optimist. And she is convinced that AI is in the process of fundamentally altering — and improving — the world.

She predicts that in ten years: “We will not recognise the world that we’re living in today in terms of the capability that’s out there. And I think that’s a remarkable thing. For all of us who are living in this technology world today, that’s what we live for. We live to build technology that can change the world. And this is uniquely that.”

More extraordinary than the present moment, though, is the fact that AMD is around to take part in it at all. When Su took over in 2014, the company looked as though it might be breathing its last breaths.

Su arrived in New York from Taiwan aged three. Her father, who had earned a place to study at Columbia University, worked as a statistician. Her mother was an accountant who later became an entrepreneur.

Su and her brother were encouraged to study hard. At MIT, Su chose electrical engineering “because it was the hard thing”, she says. A part-time job at a semiconductor lab “doing grunt work for graduate students” first exposed her to semiconductors.

She was instantly hooked. “I was taking little two-inch wafers and putting them in machines and having them do things,” she recalls. “I just thought it was the coolest thing on the face of the planet, that you could build all of this intelligence into these little chips that were the size of a quarter.”

After earning a PhD in electrical engineering, she landed a job first at Texas Instruments and then IBM, where she spent 14 years moving up the ranks. Freescale Semiconductor, a spinout from Motorola, hired her as technology chief before she was poached by AMD in 2012. She was appointed chief executive two years later. “That was a difficult time for the company,” she says.

Founded in the late 1960s at about the same time as, and down the road from, Intel, AMD was what one analyst called the “perennial runner-up”.

While Intel became the industry standard, AMD pumped out inferior chips. It existed in the mediocre middle. A corporate overhaul by Su’s predecessor was stalling; its market value had sunk to just $3 billion.

Forrest Norrod, head of AMD’s data centre, was Su’s first hire. He recalls: “After I joined I cannot tell you how many dozens of calls I got with people saying, ‘What the heck did you just do? AMD is irrelevant.’”

An engineer at heart, Su made a few bold moves. She pulled the plug on AMD’s core line of central processor units (CPUs) for data centres and redesigned them from scratch, effectively exiting a market so that it could then re-enter years later with a better product.

The revamp, which took years to deliver, paid dividends, allowing AMD to undercut Intel with a new design that was cheaper and better performing.

"In ten years, we will not recognise the world that we are living in today

Its chips started gaining share in the markets for laptops as well as data centres, which were booming even before AI, as companies put more of their data in the cloud.

In 2022, the unthinkable happened: AMD leapfrogged the market value of Intel, the company in whose shadow it had operated for half a century.

Abhi Talwalkar, a former Intel executive and AMD board director, said one of Su’s strengths is being able to pull people along, even when the ultimate goal seems impossible. “Great leaders will get the job done, push the team hard, and the team will sign up over and over again, versus leaving a bunch of dead bodies behind,” he says.

“She sets a high bar and has high expectations. She pushes people hard but at the same time, her sleeves are rolled up.”

The results have been remarkable. Since taking over, AMD’s value has grown 55-fold. Thanks to her share options, Su is worth well north of half-a-billion dollars.

The day we meet, she sold a cool $37 million on the market. Her turnaround has been turned into a Harvard Business School case study.

But now the hard work starts. In 2017, she told her engineers to start developing a new line of graphics processing units (GPUs), the specialised chips used mostly in video games, amid early signs that they could be useful for AI systems.

She doubled down in 2022, redirecting huge resources to launch a product powerful enough to grab share in the soon-toboom AI industry. That bet has also paid off. Its data centre operation saw sales nearly double to $12.7 billion last year, driven largely by GPUs.

But the mountain in front of her is perhaps taller than the last. Nvidia has over 90 per cent of the GPU market. Last year its sales were $130 billion, a fivefold increase from two years before.

Su and AMD once again find themselves the underdogs but the opportunity is vast. AMD reckons the market for AI chips could hit $500 billion by 2028. Having watched her pull off the trick once, Talwalkar is confident she can do it again.

“The company went through a remarkable pivot a number of years ago, directing so much of the company’s attention and resources to AI, to really mount a similar game plan that was executed versus Intel, now versus the big player in AI in Nvidia,” he says. “I think customers are starting to see history repeat itself.”

Time will tell, Su says. “I like to say that the bets that you make in technology, you won’t know for three to five years whether you made the right ones.”

For evidence, she need look no further than her rear-view mirror, where Intel is falling further behind. It recently laid off 24,000 people, a fifth of its workforce, and last week faced the ignominy of being part-nationalised by the US government.

Few know as well as Su how the mighty can fall. “Just because you were good yesterday,” she says, “doesn’t mean you’re going to be good tomorrow.”